Small Fed Move Doesn't Mean You Can't Buy a Homehttp://o.aolcdn.com/dims-shared/dims3/GLOB/crop/2946x1958+0+736/resize/640x426!/format/jpg/quality/85/http://hss-prod.hss.aol.com/hss/storage/midas/af8f7fd3a5925145907507e6f1dc171f/203152407/488244276.jpg

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Thursday, December 24, 2015

On the road! Man converts 189-square-foot school bus into a home — see inside

They say home is where the heart is, and for 29-year-old Patrick Schmidt, that can be literally anywhere across the country thanks to a 1990 school bus he lovingly converted with his parents.

CLICK HERE FOR THE REST OF THE STORY

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

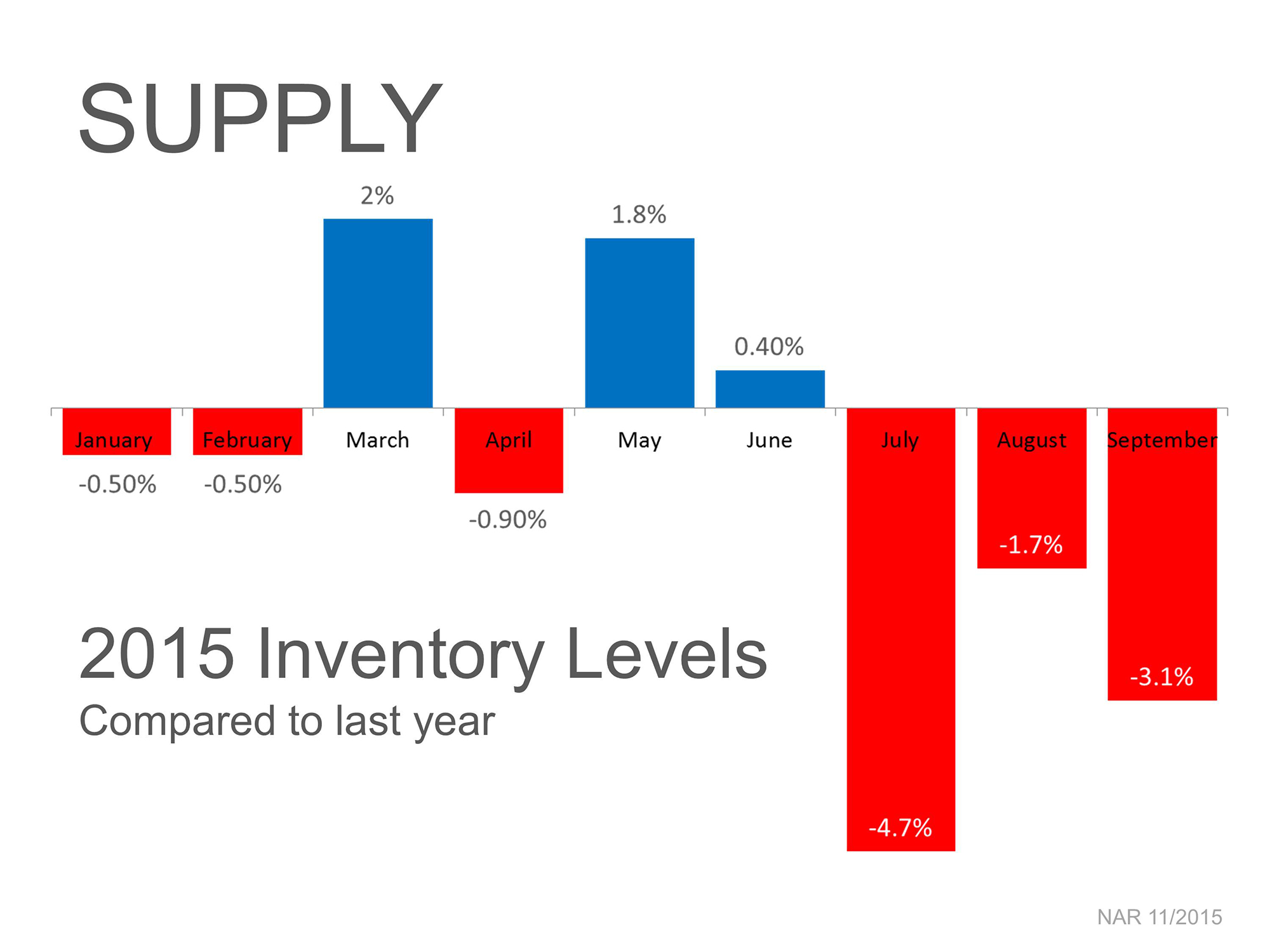

Monday, December 21, 2015

DOWNERS GROVE REAL ESTATE taking the first step

CLICK HERE TO GET STARTED

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Dupage county

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Dupage county

Wednesday, December 16, 2015

The Fed just raised rates! What does that mean for my mortgage? - Quartz

For the full implications of the Fed’s decision, see Quartz’scomprehensive explainer from Tuesday (Dec. 15). But right now let’s narrow the focus: What does an increase in the federal funds rate mean for your mortgage?

If you’re a home owner with a standard 30-year fixed-rate mortgage:

Nothing! That’s the beautiful thing about the “fixed rate”

CLICK HERE FOR THE REST OF THE STORY

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Monday, December 14, 2015

Here's why 2016 will bring good news for potential homebuyers | 2015-12-14 | HousingWire

Here's why 2016 will bring good news for potential homebuyers | 2015-12-14 | HousingWire

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Saturday, December 12, 2015

Dick Portillo, daughter-in-law rehabbing, flipping houses - Residential News - Crain's Chicago Business

CLICK HERE FOR THE REST OF THE STORY rehabbing, flipping houses - Residential News - Crain's Chicago Business

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Thursday, December 10, 2015

8 Ways the Federal Funds Rate Hike Could Affect You

A bump of 0.5% in your interest rate would raise your principal and interest payment to approximately $912/month. Therefore, a jump in mortgage rates could not only decrease mortgage affordability but shut some potential buyers out of the housing market completely.

CLICK HER FOR THE REST OF THE STORY from liz Bandstra

CLICK HER FOR THE REST OF THE STORY from liz Bandstra

Monday, November 23, 2015

{kind=link}

Friday, October 16, 2015

Foreclosure crisis lingers: Repossessions spike 66%

New foreclosures may be back to nearly normal, but the mess from the epic housing disaster in the last decade is far from gone. Bank repossessions, the final stage of the foreclosure process, jumped 66 percent year over year in the third quarter of this year, according to RealtyTrac, a foreclosure sales and analytics company. It's the largest annual rise ever recorded in bank repossessions by RealtyTrac. More than 123,000 homes went back to the bank in just three months.

New foreclosures may be back to nearly normal, but the mess from the epic housing disaster in the last decade is far from gone. Bank repossessions, the final stage of the foreclosure process, jumped 66 percent year over year in the third quarter of this year, according to RealtyTrac, a foreclosure sales and analytics company. It's the largest annual rise ever recorded in bank repossessions by RealtyTrac. More than 123,000 homes went back to the bank in just three months.CLICKHERE FOR THE REST OF THE STORYfrom yahoo

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Saturday, October 3, 2015

October Is the Best Month to Buy a Home | Money.com

“On average, October buyers get a 2.6% discount below estimated market value,” says Daren Blomquist, RealtyTrac vice president. “It’s that middle month between the summer selling season and the holidays [when] people are trying to squeeze in a purchase or a sale.”

“On average, October buyers get a 2.6% discount below estimated market value,” says Daren Blomquist, RealtyTrac vice president. “It’s that middle month between the summer selling season and the holidays [when] people are trying to squeeze in a purchase or a sale.”CLICK HERE FOR THE REST OF THESTORY from TIME

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Saturday, September 26, 2015

DOWNERS GROVE REAL ESTATE

Voted Chicago's number one real estate website for years in a row

Search for every property in the Chicago area by clicking on the link below

CLICKHERE TO START YOUR CHICAGO AREA HOME SEARCH by baird warner

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Search for every property in the Chicago area by clicking on the link below

CLICKHERE TO START YOUR CHICAGO AREA HOME SEARCH by baird warner

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Thursday, September 17, 2015

How to Spot a Bad HOA | Realtor Magazine

our buyers can avoid their own homeowner association horror story by keeping an eye out for these items during the search.

What’s the difference between a good, mediocre, and downright bad homeowner association? It’s not entirely a matter of opinion. There are specific items to look at and questions to ask that can tell your buyers whether they’re buying into an HOA that will only give them headaches. This information is particularly important in condominiums, where the HOA usually is responsible for maintaining the exterior of the buildings. If they aren’t careful, your buyers could face paying a big special assessment for years of neglected capital improvements after they close. The bill they’re typically stuck with could be anywhere from $1,000 to $30,000. (In some cases, they've gone over $100,000!) Help your buyers perform due diligence before closing by assisting them in identifying issues to minimize the element of surprise. While this isn’t intended to be legal advice and there may be other items to look at other than those mentioned in this article, this should give you ideas for how to advocate for your buyers when dealing with HOAs.

Look at the Community as a Whole

Is it run-down? Don’t solely focus on the one property your buyer is purchasing. When the HOA is responsible for maintaining the buildings, check out neighboring units and common spaces along with the home your buyer is purchasing. Here are some telltale signs of an HOA that isn’t on top of its responsibilities:

- Are the fences rusting?

- Are the building signs in disrepair?

- Does the asphalt look like gravel?

- Are the pool and other amenities clean and in good working order?

- What is the age and condition of the roofs?

- Do the buildings need to be painted?

- Are there staircases and balconies in poor shape that the HOA is responsible for maintaining?

- When were the buildings last treated for termites? Have they been neglected, with a higher risk of unknown termite damage throughout the community?

- Are there problems with siding?

- Are there grading issues causing flooding?

- What is the condition of the gutters, fascia, and other fixtures?

CLICKHERE FOR THE REST OF THE STORY FROM JIL SCHWEITZER

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Tuesday, September 15, 2015

Dos and Don'ts of Appraiser Communication | Realtor Magazine

Dos and Don'ts of Appraiser Communication

Forget the rumors that you have to keep silent. But that doesn’t mean your communications still can’t get you in trouble.

Real estate professionals and appraisers both play an essential role in the process of buying or selling a home. It is critical that these two parties work together to ensure that an appraiser provides an independent, impartial, and objective opinion of value that accurately reflects the marketplace. However, we often hear from brokers and agents that they’re unaware of how much interaction they may have with an appraiser, what they’re allowed to say, and what information they can provide. Some incorrectly believe that they are prohibited from speaking to an appraiser at all.

In reality, qualified and competent appraisers welcome any information that helps them do their job. In fact, we at The Appraisal Foundation encourage brokers to actively communicate with appraisers in a professional and productive manner. Real estate professionals should feel empowered to supply relevant materials, including the terms of the sale, applicable comparable sales, and any evidence of notable renovations done to a home that might affect its value. Additional useful data could include records that categorize maintenance and upkeep done to a home, such as regular inspections or replacements of major appliances. These materials will help an appraiser arrive at an opinion of value that accurately reflects the market value of a home.

However, real estate professionals are legally barred from any communication with an appraiser that is intended to unduly influence the outcome of the appraisal. While it might be obvious that coercing an appraiser is off-limits, it is always a good idea for agents and brokers to make sure an appraiser or regulator couldn’t interpret their communications as an attempt to improperly influence an appraisal. An example of improper communication would be asking an appraiser to provide a valuation that matches the asking price of a particular home. Another example could be telling an appraiser he or she will not receive future assignments if the appraisal does not facilitate a transaction.

And communication between appraisers and real estate professionals doesn’t have a specific cut-off point, either. A broker or agent who has questions or concerns about an appraiser’s final report may take formal steps to communicate those concerns and ask for reconsideration of the appraisal report. For instance, a broker can submit additional comparable sales through the lending institution for the appraiser to consider. A broker can also request that the appraiser correct any errors in the report, such as the miscalculation of the number of bedrooms in a home or the total square footage. The appraiser can be asked to provide additional detail explaining how he or she arrived at certain conclusions and the ultimate opinion of value. However, a broker cannot dispute an appraisal simply because he or she is not pleased with the outcome.

At the most basic level, it’s important for real estate professionals to recognize that it’s the duty of competent and qualified appraisers to provide credible opinions of value for homes. Any information that assists an appraiser in that objective is not only allowed, it is welcomed.

CLICK HERE FOR THE REST OF THE STORY FROM david bunton

Wednesday, August 26, 2015

4 Things to Know Before Buying a Home in a Homeowners' Association

CLICK HERE FOR THE REST OF THE STORY

So you want to purchase a home in a community with a homeowners’ association. Many homebuyers love the idea of enforced community appearance, included maintenance like snow removal, recreational amenities, and association management, but here are a few things you should consider when planning to purchase a home within an HOA.

Wednesday, August 19, 2015

American Housing Survey Highlights Home Buyer Preferences | NAHB Now | The News Blog of the National Association of Home Builders

If you have ever wondered what drives a home buyer to select a particular home look no further. The American Housing Survey provides insight into the home buying process, and NAHB economist Heather Taylor broke down the data in a recent Eye on Housing blog post.

The survey shows the top two reasons for choosing a home were its size (cited by 76% of buyers) and room layout/design (74%). The house’s price and the neighborhood were each cited by 72% of home buyers.

For buyers of new homes, room layout/design, neighborhood, exterior appearance and construction quality tended to be even more important than for other types of buyers. Among first-time buyers, on the other hand, price was more often a consideration (see Graph 1 below).

ACLICKHERE FOR THE REST OF THE STORYfrom american Housing Survey Highlights Home Buyer Preferences | NAHB Now | The News Blog of the National Association of Home Builders

American Housing Survey Highlights Home Buyer Preferences | NAHB Now | The News Blog of the National Association of Home Builders

What Drives a Buyer to Select a Particular Home?

If you have ever wondered what drives a home buyer to select a particular home look no further. The American Housing Survey provides insight into the home buying process, and NAHB economist Heather Taylor broke down the data in a recent Eye on Housing blog post.

The survey shows the top two reasons for choosing a home were its size (cited by 76% of buyers) and room layout/design (74%). The house’s price and the neighborhood were each cited by 72% of home buyers.

For buyers of new homes, room layout/design, neighborhood, exterior appearance and construction quality tended to be even more important than for other types of buyers. Among first-time buyers, on the other hand, price was more often a consideration (see Graph 1 below).

CLICKHERE FOR THE REST OF THE STORY

Wednesday, July 22, 2015

8 Things Millennials Want in a Home

The Millennial generation represents the largest share of homebuyers, according to a generational trends report by the National Association of REALTORS®. Weighing in at 32 percent of homebuyers, millennials are looking for different needs in a home than their predecessors. According to REALTOR Magazine®, these are the top wants of millennial homebuyers.

Affordability

Millennials are spending-savvy, especially when it comes to their home purchase. After seeing parents reel from the recession and facing the repayment of their own student loan dent, millennials want affordable, budget-friendly houses without going into their maximum approved purchase price.

Efficiency

Via Pinterest

This generation is extremely waste-conscious. With that being said, they're looking for homes in which every space has a purpose.

Flexibility

Millennials see their homes as an extension of the rest of their lives, not just a place to go after work. So they want casual and flexible spaces in a home that can be customized to fit their needs, whether that be a play room for their children, a home office, a home gym, man cave, or an extra bedroom.

"Green" Homes

Via Pinterest

Ten percent of millennials who purchased a newly-built home said they purchased new for green/efficiency reasons, according to an NAR study. Think new appliances, sustainable building materials, and energy-efficient LED lighting.

Entertaining Possibilities

Via Pinterest

It's no surprise that this generation of homebuyers want their homes to be a hub for entertaining family and friends. Open floor plans, fire pits, game rooms, outdoor living spaces, and "man caves" appeal greatly to millennials.

Location, Location, Location

These young homebuyers place importance on being close to urban necessities and entertainment. Home serves as a base for these active homebuyers and they're willing to compromise home size in order to be closer to certain amenities.

Move-In Ready

Growing up in the age of technologic advancement, millennials are accustomed to having things done in an instant. This generational trait transitions into their housing preferences, as well. The more a seller has done, the better. Millennials want updated and upgraded homes, and they want it done before they move in.

Maintenance-Free Materials

Millennials work long hours and have lots of interests outside of the home, so materials that require minimal time and care are key. For example, they prefer tile, laminate or vinyl flooringthat mimics wood over the maintenance of the real thing.

Overall, the Millennial generation doesn't view their home as a status symbol but as long-term investment that will suit the needs of their busy and active lifestyles now and evolve with each life stage.

If you're interested in purchasing your first home, download our free Mortgage 101 Handbook, a great resource of all things home buying and financing for first-time buyers.

8 Things Millennials Want in a HomeCLICK HEREFOR THE REST OF THE STORY

Tuesday, July 14, 2015

Despite Rising Prices, 63 Percent of Properties Sold at a Discount in May 2015

Despite Rising Prices, 63 Percent of Properties Sold at a Discount in May 2015

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Wednesday, July 8, 2015

7 Negotiating Tips for Homebuyers | Real Estate Tips | HGTV

Remember these tips during the deal-making process of your home purchase.

QUICK ON THE UPTAKE

It is critical to respond to counteroffers as soon as possible and to avoid making a counteroffer with any term that is not truly a deal breaker. Delays in responding leave space open for another buyer to step in and create a bidding war, or even more likely, for the seller to perceive that other serious buyers might be out there. A seller's mere perception of a hint of a whiff of the scent of a potential bidding war is a homebuyer's number one nemesis, ratcheting up the possible sales price in the seller's head on an exponential basis.

It is critical to respond to counteroffers as soon as possible and to avoid making a counteroffer with any term that is not truly a deal breaker. Delays in responding leave space open for another buyer to step in and create a bidding war, or even more likely, for the seller to perceive that other serious buyers might be out there. A seller's mere perception of a hint of a whiff of the scent of a potential bidding war is a homebuyer's number one nemesis, ratcheting up the possible sales price in the seller's head on an exponential basis.

#2: CUT IN THE MIDDLE (WO)MAN

When you want to ask or tell the seller something, always always always go through your real estate agent, who will communicate your request or concern to the seller's agent. I know it seems inefficient, but it is truly a rookie move to contact the seller directly. It's just not done, mostly because the terminology is tough to master and legally sensitive. Also, some seemingly innocent and minor changes to your agreement with the seller might create problems with your lender; your real estate agent is better equipped than you to see these red flags. You hired your agent, so use him/her! It will prevent the catastrophic misunderstandings (read: drama) that can result when you or the seller says something even slightly different than what you each actually mean!

When you want to ask or tell the seller something, always always always go through your real estate agent, who will communicate your request or concern to the seller's agent. I know it seems inefficient, but it is truly a rookie move to contact the seller directly. It's just not done, mostly because the terminology is tough to master and legally sensitive. Also, some seemingly innocent and minor changes to your agreement with the seller might create problems with your lender; your real estate agent is better equipped than you to see these red flags. You hired your agent, so use him/her! It will prevent the catastrophic misunderstandings (read: drama) that can result when you or the seller says something even slightly different than what you each actually mean!

#3: GAUGE THE SITUATION WHEN DEALING WITH A DEVELOPER/BUILDER

A lot of this talk about negotiating and price and terms, etc. may be moot when you're buying a newly built home. By and large, the builder/developer dictates the terms on which they will sell you a home in their community, and you either take it or leave it. The list price is the price you pay, though in many markets, developers and builders are willing to negotiate if they have a large amount of inventory.

The builder will have a standard contract with a standard required deposit, standard contingency removal or objection periods, and a standard set of disclosures that they make to every buyer. The larger the builder, the more set they will be in their ways and to their price. That said, it doesn't hurt to ask for concessions or upgrades. Furthermore, builders hate getting sued, so they generally try to create a standard contract that affords you most or all of the same protections your real estate agent would build into a contract for you.

A lot of this talk about negotiating and price and terms, etc. may be moot when you're buying a newly built home. By and large, the builder/developer dictates the terms on which they will sell you a home in their community, and you either take it or leave it. The list price is the price you pay, though in many markets, developers and builders are willing to negotiate if they have a large amount of inventory.

The builder will have a standard contract with a standard required deposit, standard contingency removal or objection periods, and a standard set of disclosures that they make to every buyer. The larger the builder, the more set they will be in their ways and to their price. That said, it doesn't hurt to ask for concessions or upgrades. Furthermore, builders hate getting sued, so they generally try to create a standard contract that affords you most or all of the same protections your real estate agent would build into a contract for you.

CLICK HERE FOR THE REST OF THE STPRY FROM | HGTV

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Thursday, July 2, 2015

20 Questions To Ask Before Hiring Rental Property Management!

I get this question a lot from real estate investors and it came up recently on the BiggerPockets.com forums. “How do I know if a property management company is any good?” My answer always comes back to the questions you are asking the company you are getting ready to hire. Before you will know if they are any good at the service you are looking for, you have to know the right questions to ask. I have been advising real estate investors to ask these same 20 questions for years and so far, they have helped keep many investors out of trouble.

Sunday, June 21, 2015

Cool Down Your Home Naturally « Baird & Warner

Cool Down Your Home Naturally

August 15th, 2014Seeing those summer electricity bills roll in is the last thing we want during our relaxing summer days. But there are ways to trim down on that expense without breaking a sweat. Here are a few ways to cool down your home naturally.

Pull down the shades. If you’ve ever taken a magnifying glass to an ant hill on a sunny day, it should be pretty easy to enlarge that image and apply it to your home. The windows to your house act as that evil magnifying glass, frying the inside with scorching sun rays. Placing some blinds or curtains over your windows can significantly cool down your home at a much quicker pace.

Keep appliance usage to a minimum. Your dishwasher, dryer, stove, microwave all have one thing in common — when they’re on, they generate heat. The less you use these secondhand heat generators, the cooler your home will be. It’s unrealistic to quit all of these appliances cold turkey, but doing small things like letting your clothes to air dry outside can make a huge difference.

Crack the windows at night. The temperature is always at its lowest during the night time — sometimes the summer will go as long as 50 degrees. Take advantage of those nights and let the cool air in. No fans or A/C are required

Crack the windows at night. The temperature is always at its lowest during the night time — sometimes the summer will go as long as 50 degrees. Take advantage of those nights and let the cool air in. No fans or A/C are requiredCLICK HERE FOR THE REST OF THE STORY FROM « Baird & Warner

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Before You Install a Retractable Awning - New York Times

DECKS and patios are popular gathering places, that is, of course, until scorching sun or annoying drizzle forces folks inside.

Tom Bloom

It is possible, though, to get more use from a deck or patio by installing a retractable awning.

“There are two basic options for homeowners who want a deck or patio awning,” said Ido Eilam, the chief executive of SunSetter Awnings in Malden, Mass., “manual or automatic.” Manual awnings must be hand-cranked open or closed; automatic awnings use a motor to do the work, but are more expensive.

Mr. Eilam said that about 70 percent of SunSetter awnings were sold directly to consumers and that a homeowner with a minimal amount of skill should be able to install an awning in a couple of hours. An instructional DVD is included.

A basic 16-foot-wide-by-10-foot-deep SunSetter awning costs about $1,330 with a hand crank or about $1,650 for a motorized version. Retrofit motor kits are about $300.

Howard Falkow, the owner of Better Living Sunrooms in Baldwin Place in Westchester County, said that he recommends awnings that have both a motor — for convenience — and a manual crank that allows for opening and closing if the power goes out. He said that a good retractable awning should not need ground supports to hold it up and that shoppers should look for models made from extruded steel rather than lightweight aluminum.

A 16-by-10-foot extruded steel awning from Mr. Falkow’s company costs about $3,500, including installation.

CLICK HER FOR THE REST OF THE NEW YORK TIMES STORY

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Thursday, June 18, 2015

Home buyers to get simpler forms under new federal mortgage rules reated by the Consumer Financial Protection Bureau - Residential News - Crain's Chicago Business

HCLICK HERE FOR THE REST OF THE STORYome buyers to get simpler forms under new federal mortgage rules reated by the Consumer Financial Protection Bureau - Residential News - Crain's ChicagBig changes in the process of buying a house kick in Aug. 1, the day new federal mortgage rules take effect that are designed to eliminate closing-day surprises or confusion.

• Both forms emphasize clarity.

• Both forms emphasize clarity.

While title companies and real estate agents and lawyers are scrambling to be ready by the deadline, home buyers should feel more like guests at a well-executed dinner party, oblivious to the mess in the kitchen and content to be served each course at just the right time.

"It's going to bring better peace of mind that you know what you're getting into with this loan," said Ben Niernberg, executive vice president at Northbrook-based Proper Title. If all the professionals in the pipeline handle the new rules well, homebuyers should notice only that "things have gotten easier to understand," he said.

For the homebuyer, the new rules created by the Consumer Financial Protection Bureau bring two key changes: All the financial details of their purchase will be spelled out more simply, and the forms containing those details will be in their hands three business days before the closing, giving them time to ask for clarity on anything they don't understand.

"You're getting time to see all the moving parts of your loan a few days before you sit down at that table to close the transaction," said Maurice Hampton, managing broker and CEO of Centered International Realty based in Beverly. CFPB says consumers will "Know Before You Owe."

RESPONSE TO SUBPRIME MELTDOWN

Enabled by the Dodd-Frank Act, the TILA-RISPA Integrated Disclosure rules, as they are known, come largely as a response to the subprime mortgage meltdown, in which some borrowers were unaware of the moving terms of their adjustable-rate mortgages and wound up in default when a rising interest rate increased their monthly payments.

While some experienced real estate buyers may see the changes as a belt-and-suspenders approach to the relatively rare problem of buyers misunderstanding their loans, eventually the changes will become transparent, say most people in real estate and related industries.

"There will be a few more steps along the way, but the steps are to protect people and give them a chance to make a better financial decision," said Tom Pilafas, executive vice president of Near North National Title Insurance in Chicago.

Here are four things to know about the changes:

• The rules apply to loan applications initiated Aug. 1 or later. Any loan in process prior to that will operate under existing rules. All-cash purchasers also are exempt.

• The rules require two new forms, both of which replace—and are intended to simplify—existing forms.

First is the loan estimate, delivered to the borrower within three days of application and projecting the monthly costs, the closing costs and the cash the borrower will need to bring to the closing. This form will take the place of a Truth in Lending, or TILA, form and the Good Faith Estimate. Second is a Closing Disclosure form, delivered three business days before the scheduled closing. This one replaces a closing-day form known as HUD-1 and a second TILA form.

"The difference with the new forms is that the figures on the first one and the second one have to agree, or be very close," said Jeffrey Baker, a lawyer with Sorling Northrup in Springfield who works for the Illinois Association of Realtors. "There was no mechanism requiring them to match up in the past."

CFPB's rules include penalties for lenders if the figures on the two forms aren't within an established range, Baker said. The idea is to prevent buyers who've fallen in love with a certain house from getting markedly more expensive terms at closing than they were counting on, "when they might feel they have to just go ahead and do it," Baker said.

• Both forms emphasize clarity."

When you closed in the past, you got a spreadsheet that was a bunch of numbered lines," said Christopher Hacker, a co-founder of ShortTrack, a Chicago-based real estate transaction software company. "It was confusing, and you needed somebody to decipher it for you." Under the new rules, "you'll see something text-based and more intuitive that tells you what you'll owe" on a monthly basis, and how that will change in the future, in the case of a loan with an adjustable rate.

• Last-minute changes in a sale will be harder to make.o Business

Thursday, May 14, 2015

How to Sell a House With Tenants

Tenants are a definite wild card when it comes to selling a home. On the one hand, there are plenty of horror stories about angry or disgruntled tenants making it impossible to sell a home. On the other hand, a tenant can be a valuable ally in the sales process if he or she is cooperative and motivated to help you sell. In the end it is up to you to gauge your landlord/tenant relationship and to decide how to best sell your home – while the tenant is residing there, or after he or she is gone.

Keep in mind that what a tenant tells you they will agree to do while you are trying to sell your home and what they actually do could be too vastly different things. Most real estate agents will tell you that having an uncooperative tenant will make selling your home next to impossible. Knowing how to sell a house with a tenant is a critical aspect of getting top dollar for your home!

Before hiring a real estate agent to sell your home it goes without saying that you should ask the tenant first if they have any interest in purchasing it. You are going to need your tenants utmost cooperation in this situation so you best respect them by explaining completely the situation you are in and why you want to sell. Giving them first dibs shows you have some compassion for their housing needs as well.

Options for Selling with a Tenant

Wait for the lease to expire

Tenants can wreak havoc on a sale. Some tenants can become angry when they discover that you are selling the home they live in. Other tenants are just not nice people to begin with. Still others are just dirty and will not keep the home in a good state for showings. If you know you have a slob living in your place you can count on this not changing when the for sale sign goes up. Once a slob always a slob. If your long term plan is to sell your home it makes sense to be extra careful when initially choosing a tenant. Let the renters know up front that your long term plan is to sell your home and get the tenants reaction. If you don’t get positive vibes you may be better off waiting for a tenant who

click here for the rest of the story

Wednesday, May 6, 2015

How To: Choose a New Roof for Your House - Bob Vila

Whether you are building from scratch or choosing a new roof for your existing home, a wide range of materials are readily available and worthy of consideration. These include asphalt, wood, and composite shingles, as well as slate, concrete, and clay tiles. Style is an important factor, but it’s not the only one. Product cost, material weight, and installation requirements should also influence your selection. Here’s what you need to know:

The Square

Before we talk materials, let’s talk terminology. Roofers don’t usually use the measure “square feet.” Instead, they talk in squares. A square is their basic unit of measurement—one square is 100 square feet in area, the equivalent of a 10-foot by 10-foot square. The roof of a typical two-story, 2,000-square-foot house with a gable roof will consist of less than 1,500 square feet of roofing area, or about fifteen squares.

Before we talk materials, let’s talk terminology. Roofers don’t usually use the measure “square feet.” Instead, they talk in squares. A square is their basic unit of measurement—one square is 100 square feet in area, the equivalent of a 10-foot by 10-foot square. The roof of a typical two-story, 2,000-square-foot house with a gable roof will consist of less than 1,500 square feet of roofing area, or about fifteen squares.

Cost

A number of considerations will affect the cost of a new roof. The price of the material is the starting point, but other factors also must be considered. One is the condition of the existing roof if you are remodeling a house—if old materials must be stripped off, and if the supporting structure needs repair, that will all cost money. The shape of the roof is another contributing factor. A gable roof with few or no breaks in its planes (like chimneys, vent pipes, or dormers) makes for a simple roofing job. A house with multiple chimneys, intersecting rooflines (the points of intersection are called valleys), turrets, skylights, or other elements will cost significantly more to roof.

A number of considerations will affect the cost of a new roof. The price of the material is the starting point, but other factors also must be considered. One is the condition of the existing roof if you are remodeling a house—if old materials must be stripped off, and if the supporting structure needs repair, that will all cost money. The shape of the roof is another contributing factor. A gable roof with few or no breaks in its planes (like chimneys, vent pipes, or dormers) makes for a simple roofing job. A house with multiple chimneys, intersecting rooflines (the points of intersection are called valleys), turrets, skylights, or other elements will cost significantly more to roof.

Materials

Not every roofing material can be used on every roof. A flat roof or one with a low slope may demand a surface different from one with a steeper pitch. Materials like slate and tile are very heavy, so the structure of many homes is inadequate to carry the load. Consider the following options, then talk with your designer and get estimates for the job.

Not every roofing material can be used on every roof. A flat roof or one with a low slope may demand a surface different from one with a steeper pitch. Materials like slate and tile are very heavy, so the structure of many homes is inadequate to carry the load. Consider the following options, then talk with your designer and get estimates for the job.

Asphalt Shingle. This is the most commonly used of all roof materials, probably because it’s the least expensive and requires a minimum of skill to install. It’s made of a fiberglass medium that’s been impregnated with asphalt and then given a surface of sand-like granules. Two basic configurations are sold: the standard single-thickness variety and thicker, laminated products. The standard type costs roughly half as much, but laminated shingles have an appealing textured appearance and last roughly half as long (typically 25 years or more, versus 15 years plus). Prices begin at about $50 a square, but depending upon the type of shingle chosen and the installation, can cost many times that.

Photo: stonecreekinsurance.com

Wood. Wood was the main choice for centuries, and it’s still a good option, though in some areas fire codes forbid its use. Usually made of cedar, redwood, or southern pine, shingles are sawn or split. They have a life expectancy in the 25-year range (like asphalt shingles) but cost an average of twice as much.

Metal. Aluminum, steel, copper, copper-and-asphalt, and lead are all durable—and expensive—roofing surfaces. Lead and the copper/asphalt varieties are typically installed as shingles, but others are manufactured for seamed roofs consisting of vertical lengths of metal that are joined with solder. These roofs start at about $250 per square but often cost two or three times that.

Tile and Cement. The half cylinders of tile roofing are common on Spanish Colonial and Mission styles; cement and some metal roofs imitate tile’s wavy effect. All

CLICK HERE FOR THE REST OF THE STORYfrom - Bob Vila

Neal Paskvan is a full time Realtor specializing in Downers grove, Darien,Woodridge, Westmont and Du page county Real Estate

Thursday, April 30, 2015

11 Tips for Refinishing Hardwood Floors - Yahoo Homes

It’s incredibly satisfying to bring your hardwood floors back to life. Whether it’s beautiful hardwood that has been hiding beneath carpet or hardwood floors you’ve had and enjoyed for years, uncovering and refinishing your floors can revitalize your home. Hardwood flooring has stood the test of time, stylistically and literally, because of its ability to be refinished.

")

(Credit: patrisyu/Shutterstock)

Here are 11 aspects of the process you may not have known about.

1. Three Types of Finish

There are three kinds of finishes you can choose from for your floors.

Polyurethane, oil- or water-based. Polyurethane has varying degrees of luster with a plastic-looking finish. It can darken or yellow the wood over time, though some new formulas don’t affect the wood as much. While good for high-moisture or high-traffic areas, it can be extremely difficult to spot-repair if nicked or gouged.

Polyurethane, oil- or water-based. Polyurethane has varying degrees of luster with a plastic-looking finish. It can darken or yellow the wood over time, though some new formulas don’t affect the wood as much. While good for high-moisture or high-traffic areas, it can be extremely difficult to spot-repair if nicked or gouged.

Varnish. Matte-glossy finish. Varnish comes in a variety of lusters, with the higher gloss being most durable. It darkens with age, though more slowly than polyurethane, and is easily spot repaired.

Penetrating sealer. Natural-looking finish that brings out the grain of the wood. Penetrating sealer may also darken over time, but it provides good protection, especially when waxed. It is the least durable of the finishes but the easiest to repair.

CLICK HERE FOR THE REST OF THE STORY FROM Yahoo Homes

Subscribe to:

Posts (Atom)